A new lender has entered the mortgage space, but this one’s a little unique, and its offerings are too.

You see, they’re a “marketplace lender,” otherwise known as a peer-to-peer lender, meaning everyday investors can provide funds to borrowers seeking mortgages.

The lender in question, San Francisco-based Social Finance, or “SoFi” for short, says individuals and institutional investors have the ability to “create positive social impact on the communities they care about while earning compelling rates of return.”

In other words, you can be the mortgage lender and make some money in the process. Oh yeah, and earn some good karma if you think peer-to-peer lending is an act of goodwill.

Anyway, the company has already doled out over $1 billion in student loans and now has its sights set on the mortgage market, which some seem to think has become too restrictive. Just ask Ben Bernanke…

The idea here is to target early-stage professionals (recent graduates) who need help financing their home purchases (they also offer refinancing). They are known as “HENRYs,” or High Earners, Not Rich Yet.

Basically, they have the income, but they may not have the savings for a down payment yet, thanks to student loan debt and a lack of earnings history.

SoFi Offers Interest-Only and 10% Down Mortgages with No MI

- Aside from appealing to Millennials

- And being a tech-driven mortgage disruptor

- SoFi also offers specialty home loans you won’t find everywhere else

- Like interest-only products and low-down payment mortgages without MI

I dug into their website and found some interesting stuff. For one, they offer interest-only mortgages, which are considered non-QM and somewhat harder to come by these days.

Additionally, they offer loans with as little as 10% down without mortgage insurance, which again is slightly unconventional but probably just collected via a higher interest rate.

Still, they offer IO mortgages with loan amounts as high as $3 million, meaning they’re a jumbo peer-to-peer non-QM mortgage lender.

Per their website, they currently offer a 5/1 ARM with a 10-year interest-only option, a 7/1 ARM, and a 30-year fixed.

SoFi Home Improvement Loans

- They also offer home renovation loans

- With online approval to funding in just 7 days on average

- The loans are unsecured so your home equity isn’t involved

- SoFi doesn’t charge any closing costs and payments are fixed

The company also recently launched a line of home improvement loans for those looking to do renovations on an existing property.

They do not charge origination fees or other closing costs, nor do they charge for a home appraisal.

Additionally, you can borrow up to $100,000 without any home equity. To that end, they are more like personal loans than they are HELOCs.

Borrowers can take out amounts ranging from $5,000 to $100,000 depending on their needs.

At last glance, rates ranged from 6.58% APR to 13.62%, assuming you use autopay to make monthly payments.

And terms varied from just three years to seven years and potentially longer.

They advertise fixed rates, but you might have the option of a variable rate as well.

SoFi Mortgage Rates Seem Pretty Competitive

- They seem to offer pretty attractive mortgage rates

- Relative to the competition

- And because SoFi doesn’t charge origination fees

- The rates might even be cheaper than they look

I took a look at SoFi mortgage rates on June 1st, 2018 and they appeared to be fairly competitive relative to what else is out there.

The assumptions were for an 80% loan-to-value ratio, which means 20% down payment or 20% in existing home equity. If you’re putting down less or have less equity, expect a higher interest rate.

Additionally, the 5/1 ARM assumes a 75% LTV, so you need at least 25% equity or down payment.

Sample mortgage rates from June 1st, 2018 were as follows:

– 4.375% for the 5/1 ARM with an interest-only option

– 3.875% for the 7/1 ARM

– 4.125% for the 15-year fixed

– 4.25% for the 30-year fixed

They seem pretty close to what traditional lenders are offering these days, though keep in mind that SoFi doesn’t charge loan origination fees, similar to Eave, so you need to factor in the lower fees as well, which can be a game-changer.

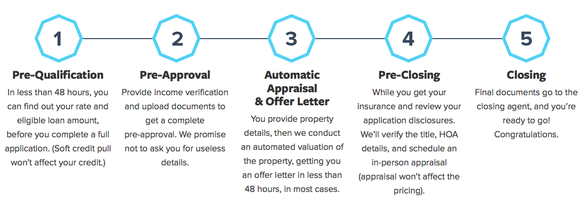

SoFi’s Loan Underwriting Is Supposedly Quick and Easy

- SoFi is attempting to speed up the home loan process

- By banking on technology

- They say they can close a mortgage in less than 21 days

- Versus the industry average of 30-45 days

Are you an ambitious professional? If so, you might be the right fit for SoFi. Even more intriguing than their product offerings is their underwriting process.

SoFi claims that they can fund a mortgage in less than 21 days, as opposed to the industry average of 30-45 days. And they promise not to ask for “useless details.”

Part of their speediness be related to the fact that they use AVMs instead of appraisals for loan approval, which can certainly save some time. However, they eventually conduct an in-person appraisal as well.

They also ask applicants to apply and upload documents online, which allows them to complete loan approvals complete with automated valuations in less than 48 hours.

SoFi Cares Where You Went to School and What You Majored In

- Because of their student loan background

- SoFi cares where you went to school

- And what you studied while you were there

- This is probably a means to keep defaults low by only going after applicants with bright futures

Of course, there is a major caveat. In order to qualify for a SoFi mortgage, you need to have graduated from a selection of Title IV accredited universities or graduate programs.

This might have something to do with the fact that they were a student loan lender before jumping into mortgages.

Not sure which schools/degrees qualify, but I think the expectation is that even if you aren’t making much money now, you’re expected to be in the near future.

I went through the beginning of the loan application process online and noticed that only certain degrees were listed. It’s unclear if it’s an exhaustive list, but they certainly take schooling seriously.

However, SoFi refers to their debt-to-income limits “flexible,” so you might be okay if income is a little light as long as you went to Stanford.

They also determine loan eligibility by credit history and employment status, and require that applicants be at least the age of majority in their state. So I take that to mean no child doctors. Sorry Doogie.

At the moment, SoFi mortgages are only available in California, DC, New Jersey, North Carolina, Pennsylvania, Texas, and Washington on owner-occupied properties, but they’re expected to reach other states soon.

For the record, if you want to become an investor in SoFi mortgages, you need to be an accredited investor, which generally means you need to have a net worth of over $1 million (excluding your primary residence) or make $200k per year.

So no, not every Tom, Dick, and Harry can become an individual mortgage lender, but those with money can.

It’ll be interesting to see if P2P lending gets more popular in the mortgage world as prospective homeowners look beyond traditional banks and lenders for financing. Stay tuned.

SoFi Is Offering Free Avocado Toast to Mortgage Customers

- Back in 2017 they ran an avocado toast promotion

- To make it really clear who they were targeting

- Young prospective home buyers

- It was a play on Millennials love for the culinary treat

This just in…in a bid to be the silliest mortgage lender out there, and perhaps appeal to disgruntled Millennials, SoFi is offering free avocado toast to customers who take out a purchase mortgage with the company in July 2017.

While it’s hardly a reason to buy a home, or take out a mortgage with SoFi specifically, it is kind of funny.

The back story is that Millennials have been accused of wasting all their money on trendy foodie things like avocado toast, dashing their hopes of homeownership.

To combat this myth, or perhaps reinforce it, SoFi is giving away a month’s worth of avocado toast to its customers for a limited time, delivered straight to their new door.

Curious how much a month’s worth is? Apparently three shipments of bread and avocados. Oh, and you get to select gluten-free or regular bread, but you have to toast it yourself…

Holy guacamole!

This is a really interesting article, Colin. I would be interested to see if you have written anything since this 2014 article. I have been working with short sale clients for the last 7 years. Thanks, Bert Gor

Sofi did no live up to the promises in the marketing material that I received. The ad stated that their rates were as low as 3.245%, 10 % down with no PMI. Subsequent to completing the application and submitting all of the requested material, I was informed that I would get a rate between 4.5 % and 5.5 %. I was shocked because my credit scores are in the low 800s and high 700s, which should qualify me for the lowest rate possibly. I was able to secure a mortgage with another company for rate of 3.625% with 10% down and no PMI. Maybe Sofi is good for student loans, personal loans or for people with bad credit, but I would suggest that you use someone else if you have good credit and are looking for a mortgage.

This article is misleading, the statement that SOFI offers a mortgage to people without FICO is not true, check below, I filled the application and here is a portion of their statement regarding that (last line):

Consents

By clicking this check box and continuing with the application process, you understand and agree that you are providing ‘written instructions’ to SoFi Lending Corp under the Fair Credit Reporting Act authorizing SoFi Lending Corp, a California Licensed Lender, to obtain information from your personal credit profile or other information from one or more consumer reporting agencies, such as TransUnion, Experian, and Equifax. You authorize SoFi Lending Corp to obtain such information solely to conduct a pre-qualification for credit.

Checking your rate will not affect your credit. However, if you are pre-qualified and then continue with your application and seek to obtain a pre-approval, we will request your full credit report from one or more credit bureaus.

David,

Maybe it’s not a FICO score, but a different credit score provider…