The California Housing Finance Agency has launched a new shared appreciation loan for home buyers.

The program, known as the “Dream For All Shared Appreciation Loan,” allows Californians to build wealth via homeownership without a down payment.

In lieu of that down payment, they must share a portion of their home’s future appreciation.

While that can be a costly tradeoff, it does eliminate the need for a significant amount of money at closing.

And by avoiding a larger loan amount or second mortgage, a home purchase can remain affordable.

Update: As of 04/07/2023, available funds for the California Dream For All Shared Appreciation Loan program have been reserved.

How the Dream For All Shared Appreciation Loan Works

In a nutshell, home buyers in the state of California can get their hands on a zero down mortgage, but they must trade a portion of future home price appreciation.

So if a prospective buyer doesn’t have a 20% down payment (or even a 5% down payment), they can take out a shared appreciation loan instead.

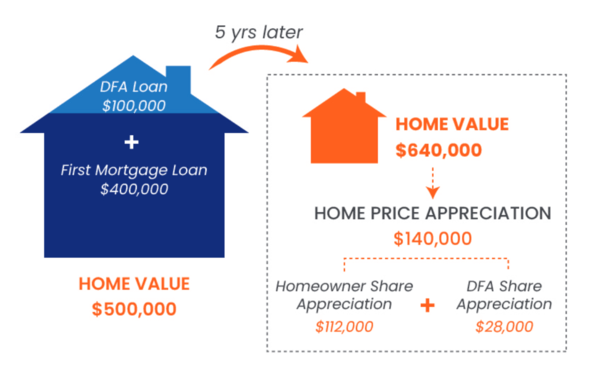

For example, if the purchase price were $500,000 they could obtain a $400,000 first mortgage at 80% loan-to-value (LTV).

Then CalHFA would provide a $100,000 DFA (Dream For All) loan that doesn’t require monthly payments.

Instead, the shared appreciation loan is paid back only when the property is sold or transferred, or the mortgage refinanced.

As a result, the homeowner would have a smaller loan amount ($400,000) and the borrower would avoid costly private mortgage insurance.

Shared Appreciation Loan vs. 3% Down Payment

| $500,000 Home Purchase | 3% Down Payment | 20% Down w/ DFA Loan |

| Loan Amount | $485,000 | $400,000 |

| Mortgage Rate | 6.5% | 6% |

| Monthly P&I | $3,065.53 | $2,398.20 |

| Mortgage Insurance | $226 | N/A |

| Total | $3,291.53 | $2,398.20 |

While other solutions exist that require just a 3% down payment, monthly costs can still be much higher.

This is driven by both a higher loan amount at 97% LTV, along with compulsory mortgage insurance for LTVs above 80%.

Together, borrowers face higher housing expenses each month, potentially putting homeownership out of reach.

The table above is an example I came up with on a hypothetical $500,000 home purchase.

As you can see, the 3% down payment results in a monthly mortgage payment of $3,291.53.

Meanwhile, the 20% down mortgage combined with a shared appreciation loan results in a monthly payment of just $2,398.20.

This is thanks to a higher mortgage rate at 97% LTV, a larger loan amount, and monthly private mortgage insurance (PMI).

That could make the home purchase unaffordable for a low- or moderate-income home buyer.

*The effective interest rate on the DFA is equal to the average annual appreciation of the home during the time it is held.

How Much Future Appreciation Is Shared?

As noted, the home buyer doesn’t have to make payments on the shared appreciation loan.

But upon sale, transfer, or refinance, they must pay off the loan and part with a percentage of appreciation.

Borrowers with incomes above 80% Area Median Income (AMI) are subject to a 1:1 appreciation share.

For example, if you borrow 20% via the shared appreciation loan and the home price increased $140,000, 20% of that total ($28,000) would go back to CalHFA.

Borrower with incomes of less than or equal to 80% AMI get a reduced 0.75:1 appreciation share.

So those borrowing 20% would only share 15% of future price appreciation, or $21,000 in their example.

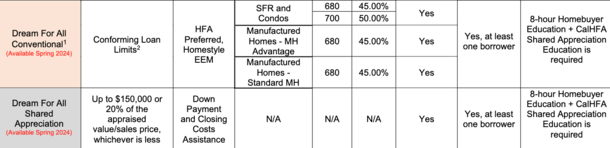

Dream For All Shared Appreciation Loan Requirements

- Must be a first-time home buyer and complete 8-hour homebuyer education course

- At least one borrower must be a first-generation home buyer

- Property must be one-unit owner-occupied house or condo

- Income limits up to 150% AMI based on CalHFA’s income limits

- Must be paired with a Dream For All conventional first mortgage

- Minimum 680 FICO for DTI of 45% and under

- Minimum 700 FICO for DTI of 50% and under

- Minimum CLTV is 70%

- Maximum CLTV is 105%

- Shared appreciation loan amount up to 20% of sales price or appraised value

To qualify for the Dream For All Shared Appreciation Loan, borrowers need to be first-time home buyers. And at least one borrower has to be a first-generation home buyer.

This generally means someone who has not owned and occupied their own property in the past three years.

Additionally, two levels of homebuyer education counseling must be completed and the borrower must obtain a certificate of completion through an eligible counseling organization.

The property must be a single-family residence (1-unit only) or an approved condominium/PUD. Manufactured housing is also permitted.

And it must be owner-occupied (no second homes or investment properties) and non-occupant co-borrowers are not permitted.

Lastly, it must be used in conjunction with the Dream For All conventional first mortgage.

Is the Dream for All Program Open to Illegal Immigrants?

There have been some provocative headlines lately claiming that illegal immigrants will be able to buy homes with nothing down, ahead of American citizens, etc., etc.

As expected, these are sensational and completely ignore the facts. Yet they still get published by major news outlets and no one seems to bat an eye.

Well, I did the research and dug in to the program specifics and the bill in question, AB 1840.

Here’s the meat of it:

“This bill provides that an applicant who meets the requirements for a loan under a CalHFA home purchase assistance program shall not be disqualified from the solely on the basis of the applicant’s immigration status.”

If we break that down, the bill simply says immigration status alone won’t be grounds for denial for the Dream for All loan program. Nothing about being illegal.

However, and here’s the most important part, the applicant must still meet all the requirements for the loan under CalHFA, including the fact that the first mortgage meet Fannie Mae guidelines.

The California Dream for All Program includes a first mortgage, which must adhere to Fannie’s underwriting guidelines, including the requirement that a borrower have a valid Social Security Number or Individual Taxpayer Identification Number (ITIN).

Additionally, borrowers must meet existing legal residency requirements. In short, the borrower must be legally in the country.

Simply put, an illegal immigrant would not fit this description.

As for why this bill exists, it’s unclear. Either the author is unaware of the complexities of mortgage lending, or simply wants to get behind something to raise his stock in the world of politics.

Or perhaps the desired language would align it with the language found in other state aid programs. But that wouldn’t change the fact that an illegal couldn’t qualify.

Are Shared Appreciation Loans Bad for the Housing Market?

While shared appreciation loans can boost affordability, they may have the unintended consequence of inflating home prices.

If buyers can’t actually qualify for a mortgage without massive help, it might mean there’s a market imbalance.

Absent accommodating programs like these, asking prices might be forced lower to better align area incomes with area home prices.

But we’ll never know if creative financing like this continues to surface, thereby keeping demand in place no matter the price.

The goal of this particular program is to increase wealth for those with low- and median-incomes, as home equity is a major driver of wealth.

However, what happens if home prices don’t appreciate like the example illustrates?

Perhaps buying a cheaper home and realizing the full amount of appreciation is a better way forward.

Regardless, with home prices still far outpacing incomes, programs like these will continue to persist.

Read more: Unison Will Provide Half Your Down Payment in Exchange for Future Appreciation

- Top Mortgage Lenders in California: UWM Sweeps All Categories, Rocket Second - April 24, 2025

- Here’s Why the Housing Market Isn’t Crashing Today - April 23, 2025

- How Will Mortgage Rates React to the End of the Trade War? - April 22, 2025

The way this is written up… they only get a share of the appreciation?? Like they could give $100k for the down payment but walk away with only $28k in your example?

I mean at this point CA is just subsidizing home ownership until the program runs out of money. Shouldn’t they get $100k back PLUS the $28k?

Andrew,

You’re saying CalHFA should get a larger share of the appreciation? They get 1:1 ratio based on down payment, so if 20% down, 20% share of appreciation. And CalHFA gets their original $100k loan back too.

This loan doesn’t help if the limited inventory results in bidding wars that make ownership still out of reach.

That’s definitely one of the main concerns with the program, potentially inflating prices with increased demand.

What happens if the owners want to sell and the home value declines? Do the homeowners owe the state now?

Michael,

I couldn’t find that scenario on their website. All I say were assumptions for home values increasing.